The Top 10 Global PR Agencies: Where Are They Now and Where Could They Be Headed

The economic fortunes of public relations agencies are typically subjected to the economic swings of national and global economies. So one would think that the last several years that have marked an uptick from the downturn of the Great Recession would have most, if not all, of the large global agencies doing quite well economically. But a look at the revenue numbers of the top 10 global PR firms indicates otherwise.

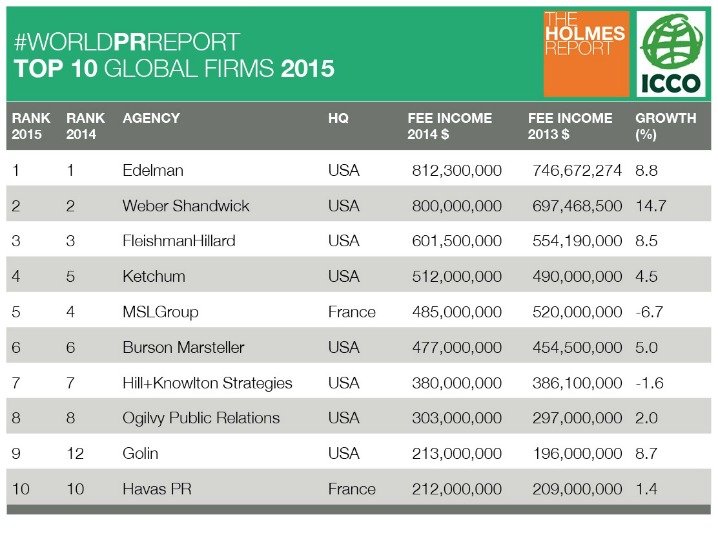

In the chart below, you’ll see the billings for these firms over the four-year period from mid-2010 to mid-2014. Brunswick and Edelman are independent, but the rest are owned by the big global media holding companies. Weber Shandwick and Golin are owned by Interpublic; Ketchum and Fleishman Hillard belong to Omnicom; Burson, Hill & Knowlton and Ogilvy are with WPP; and MSL Group is owned by Publicis. The combined billings of these top 10 global agencies is $4.78 billion — a pretty significant number considering it’s generated by just ten firms. But dig deeper and the numbers become more telling.

Here are some specific data points worth noting:

- Edelman’s model of private ownership seems to work just fine. They’ve continued to point out that as a result of not being tied to a holding company, they can control their own destiny. They have. Richard Edelman has said he wants to be a billion dollar business and with over $812 million in billings by the middle of last year, they are on track to hit that number by the end of 2016.

- Weber Shandwick seems to have figured out how to match Edelman at least fairly closely in billings. So they’ve either been allowed more free reign by Interpublic or they’ve found a leadership equation that’s paying off. With only a $12 million-plus difference between their 2014 billings and Edelman’s, they could be in a position to finish at the top by the end of 2015.

- Then there’s the middle group of Fleishman, Ketchum, Burson, H+K, and MS&L – all of which are owned by various holding companies. Burson’s growth has been flat, Ketchum and Fleishman’s have risen fairly steadily, and MSL and H+K have actually declined. (No idea how you do that in a growing economy.) Ketchum has shown the largest increase in revenue within this group, but even that appears to have tapered off last year.

- The bottom three – Ogilvy, Golin and Brunswick have seen mostly stagnant growth during the same period.

What’s interesting about this information is what it reveals about the media holding companies relative to the PR agencies they own. While they all own multiple agencies engaged in everything from PR to advertising to digital, their ability to run growing global PR firms could be seen as questionable – particularly WPP. Consider that the three agencies on the list owned by them have been experiencing extended periods of mostly stagnant growth, while other agencies owned by the other holding companies (MSL Group excluded) have been able to grow or hold their own with the economic upturn. Edelman is the outlier, not only in its growth but in its ability to grow substantially more than any single or even group of agencies other than Weber Shandwick.

But WPP is the largest media holding company in the world and the others aren’t far behind. So what’s going on here?

To get a better sense of how these companies perform economically, let’s take a look at how their stock price did during a similar period. In this case August 23, 2010 to June 30, 2014

- Interpublic — $8.54 per share to $19.39 per share

- Omnicom — $36.68 per share to $71.62 per share

- Publicis PA – $33.46 per share to $61.47 per share

- WPP — $49.95 per share to 108.49 per share

Most of these organizations were doubling their share valuation at a time when their PR agencies were experiencing modest to stagnant growth or declining. If their stock growth was tied to PR earnings alone, most of these would have been listed as DO NOT BUY or SELL.

The combination of revenue and share price points to a number of things:

- The large global agencies may not see traditional PR alone as a priority or at least as a sole source of income – this includes Edelman, which is the world’s largest PR firm. They and the other global firms (and the holding companies that own them) are continuing to diversify by adding specialized offerings like digital services, small to large ad agencies and design firms, and research entities. The agency or holding company that figures out how best to integrate these various services into a workable model will likely come out ahead of the others. That’s difficult to do when you own multiple firms that replicate each other.

- Companies that are allowed to or have the wherewithal to pursue their own future are rare, but being able to have that flexibility is no guarantee of success. Look at Brunswick – an independently owned agency that has that kind of freedom, but is in a stagnant growth path.

- Lack of growth in a growth market typically means a company isn’t providing what the market wants – regardless of what business you’re in. So one could conclude that the large firms that aren’t growing are either slowly becoming irrelevant or are in significant need of new leadership…or both.

What will be interesting is to look at the numbers four to five years from now and see if these trends have continued. More than likely one or more of these agencies will be subsumed into another to cut costs, reduce redundancy and make the parent entity more relevant. There are a number of other factors at work that could impact this scenario, but given that media holding companies are publicly traded, shareholder expectations may eventually drive the future of the agencies that can’t make their way up the revenue chart.