In an era of “fake news” is journalism at last fighting back? Taking a look back at 2017 it would appear so. Indeed, it would seem that the shocks to the media industry over the past few years are helping many organizations focus once again on quality news and investigations–in part to distinguish themselves from the mass of other, often dubious, information online.

2017 proved to be a vintage year full of reporting that made a real difference–from the The New York Times exposé on Harvey Weinstein to the ProPublica investigations of Facebook, and the Paradise Papers investigations. In terms of revenue, however, it was a mixed year that saw stronger titles pulling ahead while others faltered. The shift to reader revenue is well underway, but will not work for everyone. So what lies ahead for journalism and the media in 2018?

The report Journalism, Media, and Technology Trends and Predictions 2018, published by the Reuters Institute for the Study of Journalism with the support of Google’s Digital News Initiative, holds some clues. Based on survey responses from 194 digital leaders from 29 countries, it lays out the challenges and opportunities expected for the news industry in the year ahead.

The battle with the platforms

Concerns expressed by the respondents include increasing worry about the power and influence of platforms, especially Facebook and Snapchat. However, many publishers blamed themselves for their ongoing difficulties, citing internal factors such as resistance to change and inability to innovate.

The survey makes clear that many publishers still feel that platform companies, Facebook in particular, need to do much more to face up to their wider responsibilities. Advertisers are demanding greater transparency over measurement and for more protection for their brands. Politicians, regulators and ordinary users will be adding to that pressure. Something significant is likely to give in 2018.

According to respondents, we should also expect more news organizations to pull out of deals with Facebook, Apple, and Snapchat as they realize they are not delivering sufficient financial return.

The report also predicts that the platforms will be forced to employ armies of human internet moderators.

More focus on subscribers and personalization

Almost half the publishers surveyed see subscriptions as a very important source of revenue in 2018, more so than digital display advertising and branded and sponsored content.

To attract more subscribers, publishers say they’ll focus on podcasts and look at developing content for voice-activated-speakers. Almost three-quarters plan to actively experiment with artificial intelligence (AI) to support better content recommendations and drive greater production efficiency.

Media companies, it appears, will be actively moving customers from the “anonymous to the known,” so they can develop more loyal relationships and prepare for an era of more personalized service. Quoted in the report, Mark Thompson, CEO of The New York Times, said: “AI/intelligent assistants solving for the consumer needs across devices, environments and media is the big tech story of the year.”

The rise and rise of artificial intelligence

The report also highlighted developments to watch in this space:

Computer-driven recommendations

One of the most likely uses of AI by news publishers will be in driving better content recommendations on websites, via apps, or through push-notifications. A new recommendation service called James, currently being developed by The Times and Sunday Times for News UK, aims to learn about individual preferences and automatically personalize each edition in terms of format, time and frequency.

Assistants for journalists

Get ready for AI bots that can manage journalists’ diaries, organize meetings, and respond to their emails. Already, Replika is an AI assistant that, with a bit of training, can pick up your moods, preferences, and mannerisms until it starts to sound like you and think like you when writing text. In the future, it may be able to mimic your style of posts on Twitter and Facebook and take care of your social media while you’re asleep.

Automated and semi-automated fact-checking

AI will also assist journalists with fact-checking political claims in real time, possibly even while conducting a live radio or TV interview.

Commercial optimization

The use of algorithms to recognize patterns in data and make predictions (machine learning) is already being used to drive commercial decisions. AI-driven paywalls will be able to identify likely subscribers and, based on previous behavior, serve up the offer (and wording) most likely to persuade them to subscribe. Another use will be to create more personalized advertisements.

Intelligent automation of workflows

News organizations know they have to do more with less, without leading to journalist burn out. In the survey, 91% of respondents cited production efficiency as a “very important” or “quite important” priority this year. Intelligent automation (IA) is one way to achieve this. As examples, the Press Association in the UK has been working with Urbs media to deliver hundreds of semi-automated stories for local newspaper clients, while an automated news rewriting programme called Dreamwriter is already creating around 2500 pieces of news on finance, technology, and sports daily.

New audio platforms

Meanwhile, new devices and technologies are set to change consumer behavior, especially the rapid adoption of voice-enabled smart speakers such as Amazon Echo and Google Home. Media companies polled in the leaders’ survey said they would be investing more this year in audio-based media such as podcasts and shorter form content experiments that are native to the new platforms.

Facing an uncertain future

The report concludes with the inevitable—that the future looks uncertain. “There is no sense that the technology revolution is slowing down. If anything, it seems as if we are at the beginning of a new phase of disruption. The era of artificial intelligence will bring new opportunities for creativity and for efficiency—but also for greater misinformation and manipulation.

“Ironically, publishers know that in many ways they need to behave more like Silicon Valley tech companies, even as they try to wrest back a measure of control around distribution and strategy. That means taking risks, breaking down hierarchies and delivering higher quality products and services that audiences love. In doing this, the smartest companies will be combining data and algorithms with great content as they seek to rebuild both trust and their businesses.”

https://rossdawson.com/wp-content/uploads/2016/07/rdawson_1500x500_rgb-300x100.png00Penelope Barkerhttps://rossdawson.com/wp-content/uploads/2016/07/rdawson_1500x500_rgb-300x100.pngPenelope Barker2018-03-22 23:33:312020-06-18 03:49:35Predicting the Media Landscape: What Lies Ahead for 2018

Partly to respond to deep misunderstandings of the timeline, over the years I have many times provided deeper explanations of the timeline, including immediately after its launch. I have also long intended to create an updated timeline, adjusting the dates based on new developments since the timeline’s launch, however I have never managed to fit it in among my many projects.

However it is now the end of 2017, the year when I forecast newspapers would become insignificant in the US. It is time to review the timeline in detail, including why it was created, how accurate or inaccurate it was, and what the global news industry needs to be doing now.

The nature of the timeline

Most of the commentators and critics of the timeline seemed to have failed to read the explanatory notes included in page 2 of the original full timeline document.

“This schedule for newspaper extinction shows best estimates given current trends. The timeline is intended to highlight the diversity of global media markets and stimulate useful strategic conversations.

Newspapers in their current form becoming insignificant is not the same as the death of news-on-paper, which will continue in a variety of forms.

Ways that newspaper publishers of today will succeed in the transition beyond “newspapers in their current form” include transitioning to other channels, providing personalized news-on-paper, and tapping niche markets.”

Two key points here:

The timeline is about “newspapers in their current form”, in 2010 primarily meaning news-on-paper – news supplied on printed paper. It is NOT about news or news organizations, many of which have been successfully transitioning to delivering news in a multitude of formats other than paper.

Very importantly, it was intended to “stimulate useful strategic conversations”.

Anyone familiar with my work knows that I often say I do not believe in predictions. I am quoted in an Australian Financial Review article Futurist Ross Dawson: predictions can mislead saying:

Forecasts and predictions make Ross Dawson uncomfortable, but not for the reasons you think.

“A prediction can have negative value, by misleading people, by taking away all the uncertainties and the possibilities,” he says.

…

Rather than giving people the illusion of certainty, he believes the role of the futurist is to help people to think more effectively about the future.

“Almost all forecasts will turn out to be wrong. The future is unpredictable.”

The intent of the Newspaper Extinction Timeline

If that is how I feel about predictions, why did I make specific forecasts on the demise of news-on-paper?

The short answer is: to provoke strategic thought and action.

In 2010 I still saw enormous complacency among newspaper organizations and executives. There were a good number of news organizations that were responding in a concerted fashion to a changing world and shifting their resources to building value in new channels.

I think it is safe to say there were many more that were not taking sufficient action given the extent of the changes that were already underway, and are now regretting that they were so slow to shift their business models.

The Newspaper Extinction Timeline, by providing specific predictions, was intended to make executives think hard about the future of their industry and business, and hopefully to make them respond in ways that would create a more successful future for their organizations.

What I like about Dawson’s nudge is that it reminds us that the clock is ticking. We can’t work fast enough at the corporate level or the industry level to develop digital platforms that connect with readers and advertisers. We can’t work fast enough to build multi-media companies where print, online, mobile, iPad and others each play to their strengths and interact. Just as we were warned in the 1990s that classified advertising could disappear and we need to prepare for that, we need to be preparing today for an all-digital future — whether that comes in 2025, 2050, 2100, or some year beyond the reach of our great-grandchildren.

Here’s an interesting exercise for your management team: pick the date Dawson says your country’s newspapers will be “insignificant” and work backward. What would you need to do between today and that date to transform your business model and generate enough revenue to preserve today’s level of journalism at a sufficiently profitable level? We may all make similar choices, but my guess is the sense of urgency is more intense in the United States than India.

…

If a few dates assigned to something we’re already focused on contribute 1% additional urgency to our industry’s transformation from print to multi-media and the structure of our news ecology — with print still playing a part, even if “insignificant” — then we can thank Ross Dawson for his contribution.

I have been told about many instances in which the Newspaper Extinction Timeline has been used to help bring a sense of urgency to media boards and executives when the necessity of rapid change has not been yet recognized.

However this can cut both ways. I have been told that in one South African media conglomerate the Timeline was used to support complacency because the date given for Metro South Africa seemed very far away at 2037.

Factoring in new data

In the years following the release of the timeline I was often asked whether I had updated the timeline since its launch.

My thinking on the likely dates had certainly shifted from soon after the launch based on new data, however I never had time to do a comprehensive review of the entire timeline, and I didn’t want to make isolated changes.

However from quite soon after the Timeline’s launch two things became clear:

1. The earliest dates were too aggressive.

Seen from 2010, the forecasts of 2017 for the US, 2019 for UK and Ireland, and Canada and Norway in 2020 were certainly provocative and intended to be so. The prediction for the US is now demonstrably wrong. At his point we can fairly safely say that the forecasts for the other countries early on the list will be wrong.

However the pace of decline in news-on-paper in the countries next on the list – Finland, Singapore, Australia, Hong Kong, Denmark – suggests that those dates might still prove not to be too early.

2. Many of the later dates were considerably too optimistic (for newspapers).

Many of the dynamics in highly developed markets affecting the news industry are rapidly flowing through to developing markets. Seven years ago sustained newspaper growth in China and India seemed inevitable for the foreseeable future. However newspaper advertising in China is already falling rapidly – reportedly down 40% last year alone – as mobile usage explodes and the outlook for India may not be as rosy as suggested by headline figures.

My keynote at Arab Media Forum in 2014 was widely reported for my comments that my forecasts for the extinction of newspapers in UAE and Saudi Arabia should be revised earlier from the timeline dates of 2028 ad 2034 respectively, given the extraordinary growth of social media and mobile news in the region in the previous few years.

On various visits to countries such as Russia, India, China, and Colombia for speaking engagements I saw clear evidence that the death of news-on-paper will likely come far earlier than I anticipated in the timeline.

Wrong on US

Given it’s 2017 it is time to review the timeline’s accuracy on the state of newspapers in the US, the first country on the list.

In short, I fully acknowledge that my prediction that news-on-paper would become “irrelevant” (defined as less than 2.5% of total advertising revenue) in the US in 2017 was definitely wrong, as I have been pointedly told. But what is the actual state of the industry today?

It is very difficult to get good data on the state of the newspaper industry in the US, not least since the Newspaper Association of America (now the News Media Alliance) in 2013 stopped publishing its previously excellent industry data after 26 consecutive quarters of revenue declines.

In addition many newspaper companies globally have been extremely opaque in their financial reports, making it very difficult to assess the state of their newspapers as distinct from their digital properties.

In particular the vast majority of “newspaper circulation” figures available include both print and digital editions so tell us next to nothing about the state of news-on-paper.

Early next year we intend to add pages to examine the state of news-on-paper in other countries, beginning with UK, Canada and Australia. Please contact us if you can point us to or provide any more recent data that gives an accurate view of the picture today.

Where news-on-paper will survive (longer)

There is no doubt that in many countries news-on-paper as we usually think about it is severely endangered or rapidly getting there.

However there are a number of domains in which news-on-paper may survive significantly longer than your traditional city newspaper.

Le Monde, El País, Nikkei, The Times of India, Folha de S.Paolo and a handful of other publications are reference points globally in their language domains, so are highly advantaged relative to other publications, however cannot attract the same global audience as English-language publications.

All of these publications have been very actively transitioning to digital publication and revenue models, most with substantial success. However their position as reference publications will enable them to continue to monetize print for considerably longer than other news publications that are not in the same position. The situation of the vast majority of newspapers is not comparable to these giants.

Weekend papers

Newspapers are consumed very differently on weekdays and weekends. On weekdays they are used primarily a source of daily news, a domain where computers and mobile devices are proving to be superior delivery platforms to paper.

However weekend newspapers are consumed in a more leisurely fashion, not while commuting or in an office, with timeliness not imperative, making paper a good delivery mechanism.

Many newspapers around the world have long offered weekend-only subscriptions, an increasing number are no longer publishing every week day. So far only a handful have shifted to weekend-only production, but the shift is likely to accelerate dramatically in coming years. The traditional daily newspaper will die in many cities. The remaining weekend editions will be more akin to a weekly magazine, more focused on commentary and lifestyle than news per se.

Free commuter papers

Since Metro was successfully launched in Stockholm in 1995 and subsequently in many other European cities the number of free newspapers for commuters has exploded globally as other news organizations followed suit, with some paid newspapers going free, such as London Evening Standard in 2009.

The economics of free newspapers continues to erode, not least with a large proportion of commuters preferring to use their mobiles for news and entertainment over picking up and discarding a newspaper. Over the last years many free papers, such as News Corp’s London Paper and mX, have closed. However free newspapers are likely to continue to exist for the foreseeable future, especially in developing economies.

Community newspapers

Small community newspapers that focus on local news and identities, usually on a weekly publication schedule, are highly challenged but in some cases still have a decent runway ahead. The news is not time-sensitive and the highly defined audiences are attractive to local advertisers. Many small community newspapers are closing, however some will survive longer than city newspapers.

Revising the timeline

The Newspaper Extinction Timeline has proven to be – at least partly – wrong. So should it be revised based on the new information that has emerged since its launch?

Our intention is to revise the timeline next year if we believe doing so will create value for the industry. If we proceed we will draw on far broader input than was used for the first edition, inviting readers of this publication to share insights and perspectives so we can better estimate the pace of erosion of news-on-paper.

Creating the future of news

What frustrated me the most in the response to the Newspaper Extinction Timeline was that most people missed the point entirely.

In the big picture it is not that important if news-on-paper effectively dies. What IS critically important is that we work to create a prosperous future of news and the news industry, using whatever media and channels are the best to deliver news, engage audiences, and generate sustaining revenue.

In a rapidly changing world in which we are literally shaping the future of humanity, I believe there is no more important industry in the world than news. Individually and collectively we need to be well-enough informed to make the decisions that will create a better world tomorrow.

I also believe that it is possible, though certainly not inevitable, that we can create a positive, prosperous future of news.

We have to believe that the ‘News-powered progress’ scenario which is characterized by high-quality news and strong industry prosperity is possible in order to create it. If we don’t believe it’s possible it will never happen.

However if we do believe that it is possible somehow, the necessary next step is to work out how best to do it, by navigating the possible paths from where we are today to a prosperous future of news.

https://rossdawson.com/wp-content/uploads/2016/07/rdawson_1500x500_rgb-300x100.png00Ross Dawsonhttps://rossdawson.com/wp-content/uploads/2016/07/rdawson_1500x500_rgb-300x100.pngRoss Dawson2017-12-15 11:25:452019-03-11 12:53:24Review of the Newspaper Extinction Timeline: What We Got Wrong and the Future of News from Here

This page compiles some of the most recent available data on the state of news-on-paper in the U.S. Note that there are massive challenges to gaining an accurate current view of the state of news-on-paper.

The Newspaper Association of America (now renamed News Media Alliance) stopped providing detailed industry information in 2013.

Publicly listed news organizations have been largely very opaque in providing details on their print revenue and circulation.

Almost all so-called “newspaper circulation” figures available include both paper and digital formats. Most of the data below includes both paper and digital so does not provide real insight into the state of news-on-paper.

However the most important issue is NOT the decline of news-on-paper, but from the position we are in today how we can best create a positive future for the news industry over all channels.

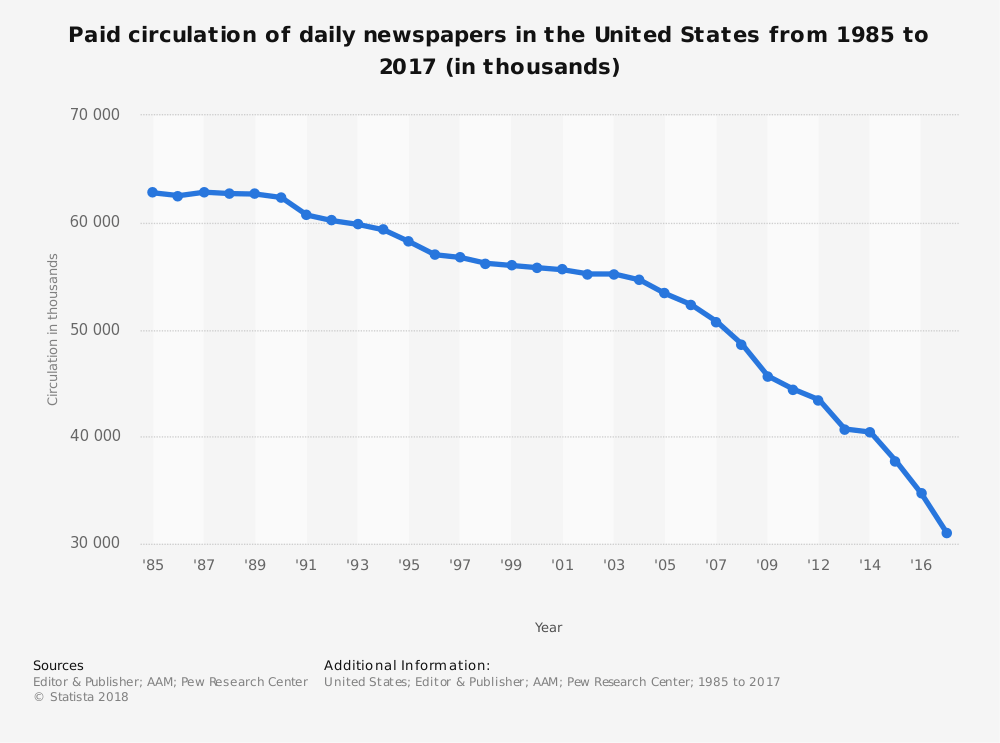

More than a 1/3 of paid daily newspaper circulation has disappeared over 10 years

At the turn of the century, newspaper circulation in the United States rested at a relatively stable level of approximately 55 million copies a year. Nevertheless, ever since peaking in the late 1980s—hitting 62.82 million in 1987—the circulation of paid daily newspapers has consistently declined.

The pace of decline accelerated in 2004 (54.63 million), but not precipitously, resulting in a drop of more than 36% by 2016 (34.66 million). According to the last ten years of recorded data (2006-2016) supplied in the chart above, paid daily newspaper circulation sunk 34%.

To take a closer look at the yearly circulation numbers, statista provides an interactive version of the chart above as well as multiple options for downloading the information.

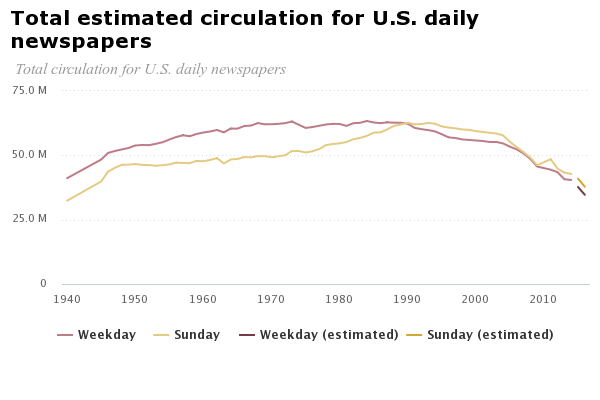

2016 circulation for both Weekday and Sunday editions has plunged to the lowest figures since 1945

The Pew Research Center offers deeper insight into the decline of newspapers in the United States, providing separate circulation data for Weekday and Sunday daily newspapers. The center’s analysis shows that in 2016 both hit their lowest levels since 1945, with circulation figures of 35 million and 38 million respectively.

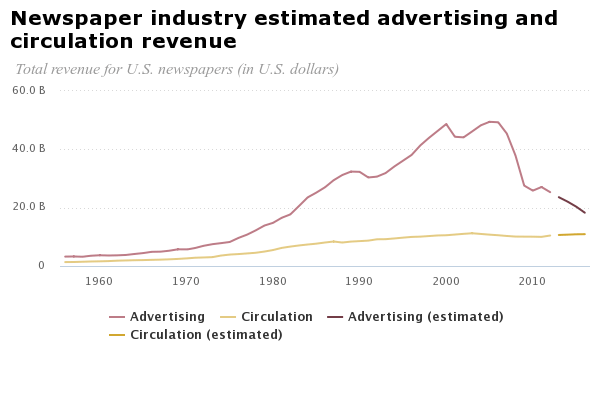

Advertising revenue dropped nearly two-thirds between 2005 and 2016, while circulation revenue rose slightly

[NOTE: Figures include both print and digital]

Data sources:News Media Alliance, formerly Newspaper Association of America, (through 2012); Pew Research Center analysis of year-end SEC filings of publicly traded newspaper companies (2013-2016). Chart source:Pew Research Center

The Pew Research Center also analyzed advertising and circulation revenue for U.S. newspapers over a 60-year period starting in 1956. Although circulation earnings have gradually increased, total advertising revenue fell significantly between 2005 and 2016. During these 11 years, total advertising revenue for the industry plummeted by nearly two-thirds, decreasing from $49 billion to $18 billion. The bulk of advertising revenue still comes from print, compromising approximately 80% in 2011 and dropping to close to 70% in 2016.

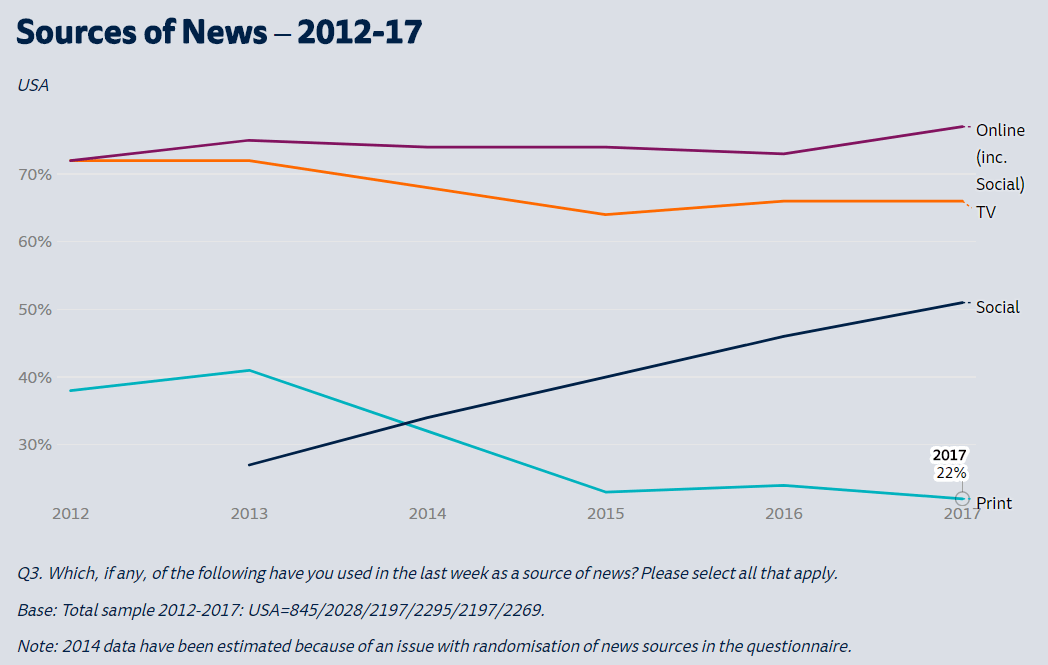

From 2013 to 2017, the number of people who read print newspapers decreased by almost one-fifth. As the medium dropped out of favor, social media as a news source enjoyed a steady climb, with consumption growing by about 6% each year.

Each year since 2012, the Reuters Institute in partnership with the University of Oxford has released a digital news report offering insights into the transition to online news and its effect on the media landscape. Although the first report covered just five countries, the latest included survey data from 70,000 participants across 36 countries.

For people wanting to delve deeper and compare data between and within countries, we strongly recommend reading the latest report and using the interactive feature to create your own charts.

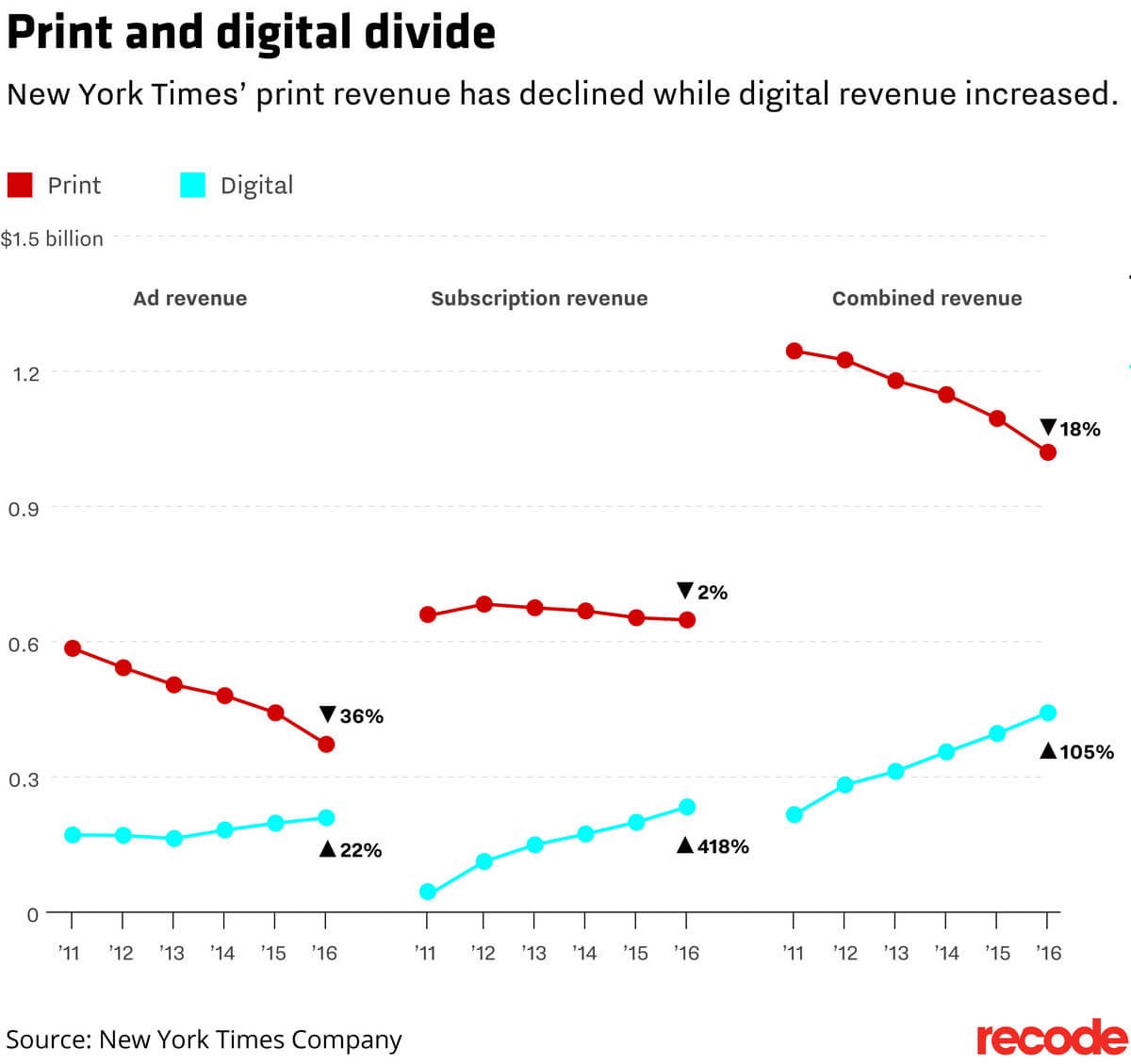

The New York Times, The Washington Post, and The Wall Street Journal are uniquely positioned to monetize print but its role is rapidly declining

The New York Times, The Washington Post, and The Wall Street Journal are distinct from other newspapers in the U.S. in that they are truly national and in fact arguably global “newspapers of record”. All three have made a concerted and successful shift to digital subscriptions and advertising. However, their role means that the role of print in their business models continues to be solid.

“The print product is a mature platform. It is, as you say, an economically important platform to us. It’s possible that platform will plateau. I think it’s more likely that the platform will eventually go away. It’ll go away because the economics will no longer make sense to us or our customers.”

Weekly community newspapers are severely challenged but are likely to have further life

There remain many newspapers across the US, primarily weekly, with small circulations but advertising revenues that are sometimes not eroding as fast as larger newspapers due to their highly geographically focused audiences and unique content.

An excellent report from Columbia Journalism Review’s Tow Center on Small-market newspapers in the digital age provides strong insights into the state of the sector and some of the ways community newspapers are successful responding to change.

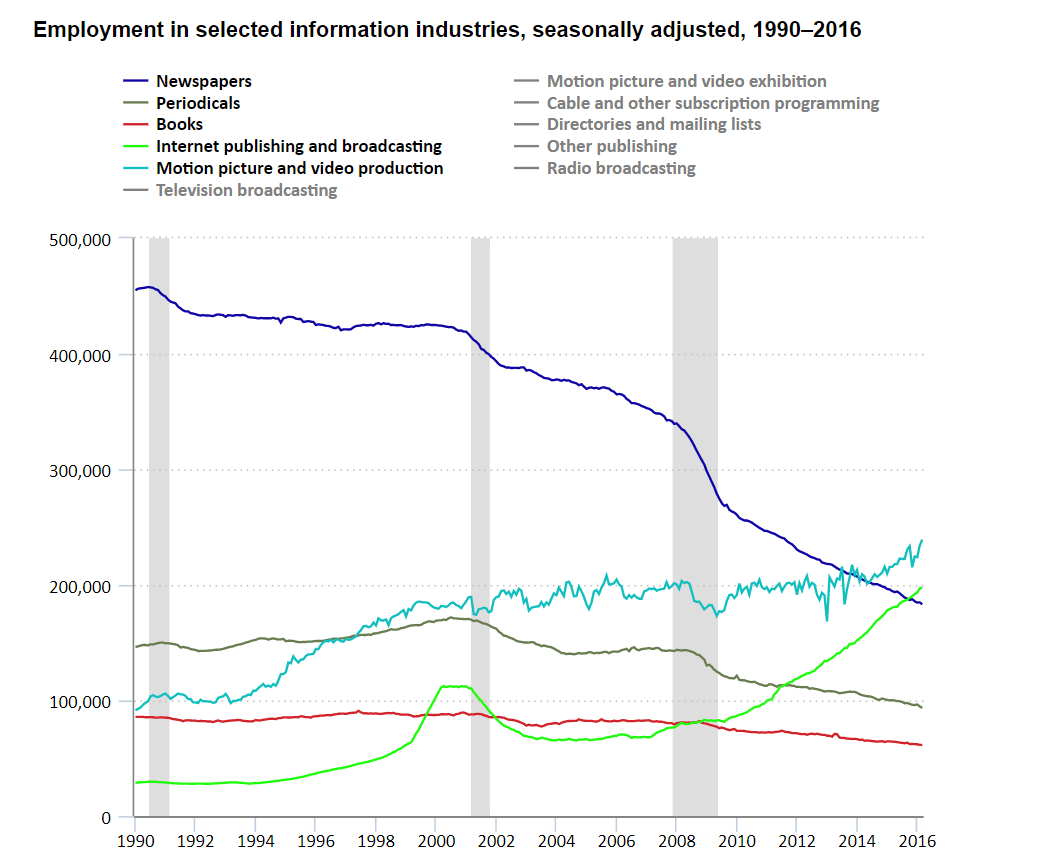

Since September 2005, employment in the U.S. newspaper industry has dropped by more than half

U.S. Newspaper employment: January 1990: 455,000 (62% decline since this date) January 2010: 260,800 (33% decline since this date) September 2016: 173,700

The U.S. Bureau of Labor Statistics also provides the above chart in an interactive format. Users can explore the data further by hovering their cursors over the lines representing the different information industries or by clicking on the “Chart Data” tab to view it in a table format.

NOTE: “Newspaper employment” includes staff working on both print and digital editions, a fraction of these figures work

https://rossdawson.com/wp-content/uploads/2016/07/rdawson_1500x500_rgb-300x100.png00Ross Dawsonhttps://rossdawson.com/wp-content/uploads/2016/07/rdawson_1500x500_rgb-300x100.pngRoss Dawson2017-12-15 09:44:112019-03-11 12:58:40Decline of News-on-paper: United States

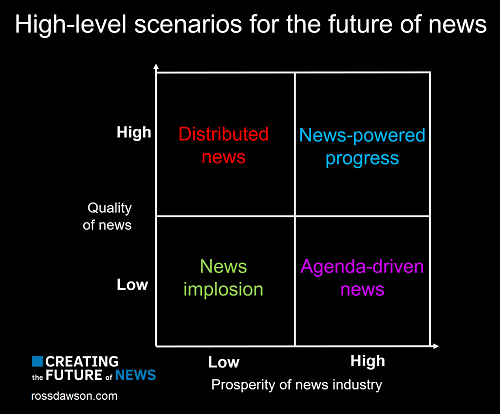

The higher the degree of uncertainty, the greater the value of using scenarios.

One of the deepest uncertainties today is the future shape of the news industry, which certainly faces deep challenges from both producer and consumer perspectives.

However it is feasible that the news industry can find its way to both strength both financially and in terms of social contribution.

This publication is framed around how we can create a positive future for news. Generating some simple scenarios on different possible high-level outcomes for the industry can help industry participants to consider both what they believe is most likely, and what they believe is possible.

Two of the key uncertainties in the future of news are:

The quality of news; and

The prosperity of the news industry.

Mapping these two variables gives us four quadrants as shown below.

Exploring these high-level scenarios allows us to examine our beliefs on what is likely or possible in the future of news. I will lay out what I see as possible across these quadrants.

You may have different opinions; in fact the true value of these scenarios is in helping to consider what you see is likely or possible in the future of news.

Distributed news

High news quality | Low industry prosperity

It is certainly plausible that we move to a world in which individuals have access to high-quality news but news organizations do not prosper. This would almost certainly be significantly based on crowdsourcing and the application of Artificial Intelligence (AI).

Crowdsourcing is not just user-generated content. In a workshop on Crowdsourcing for Media I ran in New York I identified 12 applications of crowdsourcing to news, including investigation, data gathering, fact checking, copyediting, and metadata tagging. It is also important to note that crowdsourcing is not always unpaid, as many in the media seem to think. It is participation by many people, sometimes experts, to achieve superior or more efficient results.

Blockchain could prove to be an excellent platform for getting and rewarding participation. The startup Civil provides an intriguing example of how this may work, particularly in supporting talented individual journalists.

AI is of course already being used to support journalists in structured reporting such as on financial reports and sports results. While there is significant uncertainty how fast this will progress, it is highly feasible that experienced journalists supported by AI will be able to focus their capabilities on the domains where deep investigation and insights are needed.

There are a variety of other ways this scenario could come to pass, including technological and structural mechanisms that could see efficient news delivery.

Agenda-driven news

Low news quality | High industry prosperity

On the face of it this scenario is highly unlikely, potentially implausible. Surely if the news industry is prosperous it will have sufficient resources to generate high-quality news?

This is certainly likely. However, there is the possibility that news organizations become primarily driven by specific political or social agendas, thus leading to an impoverished news landscape. It appears this trend is already developing. This could be accentuated if audiences continue to be polarized by political stance, requiring news organizations to make choices on their coverage.

Another situation that could lead to this scenario is that the companies that are reaping the most rewards from the news landscape are failing to invest in quality news, even though that could support their profitability.

News implosion

Low quality news | Low industry prosperity

This is the great fear of the last decade and more, that the rapid erosion of financial resources at news organizations leads to decreasing news quality and in turn to reducing audiences and revenue in a particularly vicious cycle. It is easy to point to the demise of many news organizations and deteriorating quality at many others as headcounts and budgets have been sliced.

This is indeed a plausible scenario, which many people seem to be taking almost as a given. However, any solid futures methodology examines the responses to trends. Responses to this scenario developing include the concerted efforts by many to drive higher quality news through technological solutions, philanthropy, crowdfunding, and other approaches.

Increasing industry prosperity could come on the other side of a dark valley in which many existing structures for news creation are lost, allowing a fresh start for new and more contemporary business models unencumbered by legacy cost structures and audience positioning.

News-powered progress

High quality news | High industry prosperity

In this world a virtuous cycle of high-quality news feeds industry prosperity and the ability to improve the news landscape to one that is substantially better than we have ever had before. Hopefully, but not necessarily, this would help create a better-informed, more proactive society that shapes a more positive future for humanity in fraught times.

This would likely to be supported by new technologies, broader distribution, high audience engagement, and broad participation in news creation to support the work of news professionals.

However there are potentially many paths and scenarios, all quite different in their detail, that could lead to this quadrant being realized.

Starting with the belief that a positive future of news is possible

The intent of my work on creating the future of news is to explore the potential paths to a world of higher quality news and higher industry prosperity. This will undoubtedly be better than one in which the industry doesn’t prosper, not least in supporting the highest possible quality of news.

The first step to creating a positive future of news is to believe it is possible. It cannot be done without that belief. That doesn’t mean that it will be inevitable or even that it will be easy, simply that it is conceivable.

From that belief we can explore how we might get there, and as an industry and society take the actions most likely to create it.

https://rossdawson.com/wp-content/uploads/2016/07/rdawson_1500x500_rgb-300x100.png00Ross Dawsonhttps://rossdawson.com/wp-content/uploads/2016/07/rdawson_1500x500_rgb-300x100.pngRoss Dawson2017-12-14 11:59:442020-06-18 03:49:35Four Scenarios to Guide Pathways to a Prosperous Future for the News Industry

The Trust Project, comprised of a consortium of news organizations and tech platforms, have a plan to win back audiences by sharing more information behind the creation of news stories online.

Staging a comeback

Led and created by Sally Lehrman, the senior director of journalism ethics at the Markkula Center for Applied Ethics at Santa Clara University, The Trust Project began growing roots in 2015 and officially launched in November 2017.

First on the agenda was to determine what consumers value in news and what makes them trust it.

Over two years, researchers conducted dozens of interviews across Europe and the United States to get the information they wanted. Then with collaborators from more than 75 new organizations, the initiative devised a set of digital standards meant to increase accountability and transparency.

Best Practices: What are your standards? Who funds the news outlet? What is the outlet’s mission? Plus commitments to ethics, diverse voices, accuracy, making corrections and other standards.

Author/Reporter Expertise: Who made this? Details about the journalist, including their expertise and other stories they have worked on.

Type of Work: What is this? Labels to distinguish opinion, analysis and advertiser (or sponsored) content from news reports.

Citations and References: For investigative or in-depth stories, access to the sources behind the facts and assertions.

Methods: Also for in-depth stories, information about why reporters chose to pursue a story and how they went about the process.

Locally Sourced? Lets you know when the story has local origin or expertise. Was the reporting done on the scene, with deep knowledge about the local situation or community?

Diverse Voices: A newsroom’s efforts and commitment to bringing in diverse perspectives. Readers noticed when certain voices, ethnicities, or political persuasions were missing.

Actionable Feedback: A newsroom’s efforts to engage the public’s help in setting coverage priorities, contributing to the reporting process, ensuring accuracy and other areas. Readers want to participate and provide feedback that might alter or expand a story.

To see an early example of the Trust Indicators applied to a news story, view this mockup.

Notably, The Trust Project’s scope extends beyond online news sites. Through partnerships with tech giants like Facebook and Google, the goal is to send such platforms machine-readable signals they can incorporate into what articles they display and how.

The following video shows how Facebook plans to display the indicators on articles in its News Feed:

Will it work?

The Trust Project’s goal to restore confidence in the news media, while cutting through misinformation and fake news, is commendable. Pairing abysmal trust scores with publishers’ rocky transition to digital (if they have survived long enough to get that far), many online news outlets are sitting in precarious positions. Implementing strategies that could both bring them more traffic and rebuild their public credibility would be like killing two very threatening birds with one stone.

However, at this point incorporating the eight core indicators may translate into little more than a well-meaning gesture.

According to Laura Hazard Owen of Nieman Lab, the first publishers that will display the Trust Indicators alongside its content will include:

From the US: The Washington Post, Mic, and The Independent Journal Review

From the UK: The Economist and Trinity Mirror (national papers include Daily Mirror, Sunday Mirror, Sunday People, and Daily Record)

From Canada: The Globe and Mail

From Germany: The German Press Agency dpa

From Italy: La Repubblica and La Stampa

The leanings of the majority of the above publications are left or center-left, excluding The Independent Journal Review, The Economist, and German Press Agency.

To complicate matters further, in countries such as the US and UK, which The 2017 Digital News Report shows have both polarized political and media climates, consumers are more likely to trust news sources that correspond to their own political leanings. This is true even though consumers in both countries show low trust levels in news outlets overall.

It is then questionable whether adding more context behind the creation of a Washington Post article would make it appear more credible to a right-wing conservative. Nevertheless, perhaps the widespread adoption of the Trust Indicators across diverse online publications could make audiences with different political views more open to reading articles from publishers they would normally avoid.

Uncertain future for tech partnerships

Tech giants Facebook, Google, Twitter, and Bing are already onboard with The Trust Project. In an article in The Atlantic published in May, Lehrman said:

“We’re already working with these four companies, all of which have said they want to use our indicators to prioritize honest, well-reported news over fakery and falsehood.”

How these collaborations will affect search engine results and social news feeds is not yet clear. Again, Owen notes that there have been no public promises from the platforms regarding whether their algorithms will give preference to publishers using the Trust Indicators.

As the small group of first wave of publishers roll them out, favoring The Trust Project collaborators could also be criticized as an unfair advantage. Small and independent publishers won’t be given the opportunity to join in the foreseeable future, which could significantly harm traffic flow from social media and search engines. However, this outcome rests on the assumption that technology platforms will, in fact, give preference to the Trust Indicators.

In the end, what’s most important about the project is the intent not only to create a standardized method to assess trustworthiness, but that this will eventually help raise the quality of online journalism overall.

Restoring public confidence in the media will be no simple task that one initiative will likely be able to tackle on its own. As The Trust Project launches and new reports and statistics on poor trust levels continue to emerge, the global media certainly has its work cut out for itself. It’s time, more than ever, to keenly monitor the impact of such strategies and keep dialogue open on how they can be improved, refined, and built upon.

https://rossdawson.com/wp-content/uploads/2016/07/rdawson_1500x500_rgb-300x100.png00Jenna Owsianikhttps://rossdawson.com/wp-content/uploads/2016/07/rdawson_1500x500_rgb-300x100.pngJenna Owsianik2017-12-13 02:53:062019-03-11 12:56:09Can The Trust Project's Plan to Win Back Audiences Work?

Facebook and Google are making conscious efforts to distinguish themselves as technology companies rather than media companies. This distinction is important to define considering their vast reach and power to shape the future news landscape.

Examining their roles becomes even more noteworthy as major news organizations around the world seek to curb the power of this duopoly. This is in part to preserve the integrity of traditional journalism and to loosen the platforms’ grip on the global ad market.

In the US, major news publishers are seeking collective bargaining rights against the Facebook-Google duopoly. The effort is spearheaded by the News Media Alliance, an organization whose members include The New York Times, the Washington Post, and The Wall Street Journal, as well as numerous regional newspapers in the US.

Similar actions are being taken in Britain. The News Media Association, representing 1,100 British newspapers, wrote a letter to Parliament calling for the regulation of the two companies for their dominance over the ad market and the massive role they play in distributing information.

Why it’s important

In 2016 Google serviced over 9 billion searches and Facebook’s user base continues a steady upward climb, reaching up to 2 billion worldwide users.

The ubiquity of these platforms and their ability to spread information to users makes them highly influential sources for news. Even more, their global reach makes them attractive platforms for publishers to use as primary hosts for originally produced content.

In a recent paper published by peer-reviewed journal First Monday, authors Philip M. Napoli and Robyn Caplan counter Google and Facebook’s resistance to the “media company” label.

In their analysis, the characterization of these companies is integral to their role in disseminating information and shaping public opinion. It also could influence the regulatory and policy rules that govern them.

What is a ‘media company’

In simple terms, a media company can be defined as an entity that deals in the mass distribution of content. According to Napoli and Caplan, there are three main criteria essential to the function of a “media company,” although they are not mutually exclusive.

The production of content; original material created by users or, in this case, news outlets.

Distribution of content by moving it from producers to consumers.

Exhibition, or the process of providing content directly to audiences.

The move toward digital news media, however, has disrupted the traditional relationship between publisher and consumer. In fact, the ease in which users or outlets can generate content and then distribute it via web-based platforms has significantly changed the media landscape.

Curation vs. creation of content

One of the central arguments tech companies use to differentiate themselves from media companies is that they do not generate content. Instead, they provide a platform for users to disseminate their own or third-party content.

For example, Eric Schmidt, the chairman of Google’s parent company Alphabet, explained, “we don’t do our own content, we get you to someone else’s content faster.” Schmidt acknowledges Google’s role in the distribution and exhibition of content, both of which are key functions of a media company as discussed above.

At a 2016 Q & A session at Rome’s Luiss University, Facebook founder Mark Zuckerberg elaborated on this view regarding his social network platform:

“We are a tech company, not a media company. When you think about a media company, you know, people are producing content, people are editing content, and that’s not us. We’re a technology company. We build tools.”

Some of these tools include Facebook Live and Facebook Instant Articles which allows users, including news publishers, to directly host content on the platform.

In refuting this argument, Napoli and Caplan claim that the lack of creation/ownership of content does not exempt a company from its role in distributing and exhibiting media content. As an example, they point to the fact that cable and satellite companies are often under the same regulatory authority as the content producers they serve. This is true even if they are not involved in the content creation process.

Human vs. algorithmic editing

A less explicit argument from Facebook and Google is that their lack of human editorial processes separates them from traditional media companies that rely on human decision-making to choose content.

However, the “gatekeeping” duty usually assigned to human editors is still being carried out, albeit in a different matter. With more media companies trying to incorporate artificial intelligence into editorial and writing processes, the argument that relying on algorithms over human editors indicates the practices of a tech rather than media company begins to hold less weight.

Can a media company be run by computer scientists?

Another argument these companies use is that the makeup of their employees distinguishes them from media companies. For example, Eric Schmidt claims that Google is a technology company “because it is run by three computer scientists”.

In debunking this argument, Napoli and Caplan comparatively look at the symbiotic evolution of media and technology over time. They state, “Technological advancements—and the associated technical expertise—have been fundamental to the media sector since at least the advent of the printing press.”

Therefore the view that the tech backgrounds of a company’s staff separates it from the media industry does not hold up based on precedent. Historically, media companies have a track record of embracing new technologies to minimize costs, increase distribution, and aid in content creation.

Duopoly pushing traditional media out of ad market

Finally, competition for ad revenue between online platforms and traditional media outlets implies that they operate within the same business sector.

According to a report by Axios, Google and Facebook are dominating the global market with about 50% of all global ad-spending going to the two companies.

In comparison with traditional media like print and radio, Google’s ad revenue alone matches that of all print media outlets globally and Facebook’s ad revenue out-earns all global ad revenue generated by radio.

Preserving high-quality journalism

Important players in the news industry are catching on to the potential negative effects of underestimating Facebook and Google’s dominance in the digital media ecosystem.

In 2016, both Facebook and Google came under harsh scrutiny for their alleged role in the spread of “fake news” during the US presidential election. As the New York Times’ Jim Rutenberg puts it, “The maneuvering is about more than the fight for digital territory. It’s about the endurance of quality journalism.”

Do Facebook and Google primarily deal in the curation of content? Yes. But with the increasingly important role these companies have in spreading news media stories, perhaps it is time for them to take responsibility for their role in affecting the quality of journalism in the future of digital news.

https://rossdawson.com/wp-content/uploads/2016/07/rdawson_1500x500_rgb-300x100.png00Jay Nelsonhttps://rossdawson.com/wp-content/uploads/2016/07/rdawson_1500x500_rgb-300x100.pngJay Nelson2017-07-23 19:22:392020-06-18 03:49:34Should Google and Facebook Be Considered Media Companies?

For years, the Indian newspaper industry has been the envy of the rest of the world. It has grown consistently since India’s economic reforms in 1990, and advertising revenues have occasionally hit double-digit growth rates, while the industry declined steadily in much of the western world.

According to a recent report released by India’s Audit Bureau of Circulations (ABC), a non-profit organization founded in 1948, newspaper circulation of its 967 member publications grew 60% between 2006 and 2016, reflecting an annual growth rate of 4.9%.

Total daily circulation for these newspapers audited by the ABC reached 62.8 million, meaning on average each newspaper boasted a daily circulation of about 65,000.

Commentators justifiably took pride in the steady growth of print newspapers, and news outlets like CNN reported on how these figures demonstrated the country’s “thriving” print media industry.

However, this positive coverage glosses over a bout of newsroom buyouts, layoffs, and shutdowns in India, notably by the English-language press and including one of the only four listed newspaper companies in the country. Few, if any, have gone beyond the headline numbers and therein lies the proverbial glass half empty.

The bigger picture

For a comprehensive picture of print media in the country, here are some other numbers to consider:

Between 2006 and 2016, average daily print circulation of the 967 publications audited by the ABC grew by 23.7 million. In the same period, India’s population grew 160 million, meaning incremental penetration of newspapers was less than 15% despite youth literacy sharply rising to 90%.

The combined annual revenues of India’s print industry declined marginally from $13.6 billion in 2013 to $13.4 billion in 2016, according to the German statistical research firm Statista.

GroupM estimates print advertising in India will grow by 4.5% in 2017, just above the previous year’s 4%, but barely above the inflation rate of nearly 4%.

The first bullet point indicates that a majority of youth (50% of India’s population is below the age of 25) may not buy into print, and may instead embrace digital news sources. The second suggests a flattening of print revenues, or even a decline in real terms, despite rising circulation.

Lastly, the third suggests near-flat advertising revenues. If these interpretations are right, India’s print industry may have hit a peak and must prepare for the slide, perhaps by embracing digital with a little more enthusiasm.

Blinded by revenue

Historically, newspapers thrived in a monopolistic position–one in which readers and advertisers had few choices. However, the Internet has broken down both walls, as we have known since at least the turn of the century. Yet the ripple effects are just beginning to show themselves in the Indian market.

In fact, the shift to digital could conceivably play out at a faster pace than it did in other countries, notably the US, for several reasons. After all, technology and newsonomics know no boundaries.

By 2020, India’s Internet users are projected to rise 60% to 730 million and smartphone users are expected to more than double to 702 million, according to a joint study by Internet technology firm Akamai and Indian software industry group Nasscom. Such rapid adoption will likely accelerate already changing reading habits.

So far, Indian print publishers, with only a few exceptions, have made only a feeble push into digital. Perhaps this seemed to make business sense because they were making money hand over fist from print, but no longer.

Most newspapers run a token website with an editorial staff that works in isolation from its print counterparts. Consequently, there is little collaboration, experimentation, or innovation in newsrooms or in marketing departments. Most publishers earn less than 10% of their revenue from online, compared to about 25% for American publishers.

Digital startups with a head start

On the other hand, a range of pure digital news media companies has emerged to tap into the fast-growing online readership overlooked by print publishers. These digital startups are also targeting the fast-growing digital advertising market, which is expected to double its share of the advertising pie by claiming 24% in 2020.

Since digital news media does not face restrictions on foreign ownership, it has allowed many global companies to throw their hats into the ring. They include New York-headquartered IBT Media and the venture-funded Scroll.in, based in Boston.

UC Web, the Chinese media company owned by Alibaba, is also in the process of setting up massive news media operations in multiple Indian languages is In addition, the British Broadcasting Corporation is in an advanced stage of adding more languages to its mix of news websites in India. Billionaire Mukesh Ambani-owned Network 18, through its ETV subsidiary, is similarly planning to start news websites in a dozen Indian languages.

Some of the pure digital startups deliver quality news stories with several multimedia elements. One, The Wire, is a nonprofit initiative. However, some are simple aggregators or rewriting shops and already have stolen a march over many print publishers’ digital offerings.

In fact, some rank among the most trafficked news websites in India, according to the web traffic-monitoring firm SimilarWeb. They include IBTimes India and Oneindia, which is venture-funded and publishes in multiple Indian languages.

India’s print publishers still have a lot going for them. They have corporate advertising support (40% vs. low teens in many other countries, according to The Economist), and generous advertising support from the federal and state governments. But they risk losing print audiences as well as digital ones, if they don’t act soon.

https://rossdawson.com/wp-content/uploads/2016/07/rdawson_1500x500_rgb-300x100.png00Bala Murali Krishnahttps://rossdawson.com/wp-content/uploads/2016/07/rdawson_1500x500_rgb-300x100.pngBala Murali Krishna2017-06-29 00:19:582019-03-01 11:12:53Why Indian Publishers Should Be Wary Despite Growing Newspaper Circulation

Online news sources have grown significantly in recent years. With this increase, more people are relying on social media sites to discover and share news stories.

According to the Reuters Institute Digital News Report of 2016, 51% of a global sample said they use social media as a source of news every week, and about 1 in 10 use social media as a main source of news.

Along with this emerging trend, access to free online platforms as well as tools that simplify the creation of websites have contributed to the spread of unverified stories. Together these factors influence the way news is discovered, consumed, and published.

This article aims to define two important media trends that have sprung up as a result: the proliferation of “fake news” and “echo chambers.” It will also provide insight into the actions of leading media companies to adapt to this changing framework and develop a new model for the future of journalism.

Defining ‘fake news’

Throughout 2016 and 2017, “fake news” was used to label misinformation campaigns that used social media and automated bots to intentionally spread false information. It has since evolved to become a toxic media brand used to describe inaccurate news.

To the alarm of many news professionals, politicians have also started using the term to undermine the credibility of unfavorable media outlets. For the sake of this article, the term “fake news” will be used to address any news stories that are simply false or purposely misleading.

According to the Reuters Institute’s 2017 trends and predictions report, by the end of the 2016 US Presidential election, there was actually higher engagement with fake news stories on Facebook than with accurate journalism (see below).

Due to the ease of sharing on social networks, untrue or exaggerated articles can spread quickly. Also, as the accepted definition of “fake news” remains ambiguous, these stories may be difficult to identify.

For these reasons, it has become increasingly important for news publishers to ensure their credibility with audiences in order to maintain a high level of integrity for their readers and to avoid being labeled as fake.

Fact-checking and data-based journalism to combat fake news

According to a 2017 report from Harvard’s Shorenstein Center on Media, Politics and Policy, the issue of fake news can addressed by three primary methods: prioritizing fact-checking, promoting bipartisan discussion, and fostering a collaborative research environment. We have already seen shifts in influential media companies to meet these goals.

At its 2017 F8 conference, Facebook announced plans to outsource fact checking to third parties like Politifact and Snopes in order to provide analysis of claims being made by news outlets online. This year, the Google Digital News Initiative (DNI) also awarded funding to projects such as the British prototype: Fact-checking Automation and Claims Tracking System (FACTS). This platform seeks to be the first to fact-check claims automatically using statistical analysis.

The same report claims, “we should seek stronger future collaborations between researchers and the media.” In addition to reducing the cost of data-based journalism, some publishers are pursuing “open-data” based platforms that focus on shared use of data, research, and user collaboration.

In 2017, Wikipedia founder Jimmy Wales announced the launch of WikiTribune. “Articles are authored, fact-checked, and verified by professional journalists and community members working side by side as equals,” states the website. The project aims to produce “evidence-based” journalism that is founded on data, research, and user collaboration.

News aggregation and user-interaction to break echo chambers

When it comes to self-tailored media, or “echo chambers,” the main causes are twofold. The first is that many people share and interact with news stories they agree with or of which they approve. In addition, social media users are free to select which media outlets to follow, and which ones to block.

The result is a potential bubble of information that may discourage engagement with challenging viewpoints.

Even more, if the view or information reinforced by these media choices are inaccurate, it may lead to a personalized information trap of unreliable sources. This has created concern among readers who don’t want to miss challenging viewpoints.

To address this issue, some consumers are turning to news aggregators. In fact, according to the Reuters Digital News Report, 57% of respondents said they prefer news aggregators in order to access a variety of sources.

News aggregators like Google News and Yahoo Japan are already quite popular with people whom prefer to receive news from multiple sources.

In China a new app called Bingdu combines news aggregation, user-driven advertisements, and Facebook-style recommendation algorithms to attract around 10 million active users.

Another Google DNI funded initiative comes from Europa Press Comunicación via a news platform that aims to “facilitate the use of open-data both as a source of news and as a fact validation instrument.”

Solutions require collaboration and innovation

The problems of fake news and echo chambers will not be solved overnight. We have already seen a shift in news production by leading media companies to ensure credibility in this changing media ecosystem. Innovative emerging publishers should continue to foster a strong relationship between publishers, readers, and researchers. This is an essential first step in building a more positive media landscape for the future.

https://rossdawson.com/wp-content/uploads/2016/07/rdawson_1500x500_rgb-300x100.png00Jay Nelsonhttps://rossdawson.com/wp-content/uploads/2016/07/rdawson_1500x500_rgb-300x100.pngJay Nelson2017-06-22 21:12:032019-03-01 11:13:55Overcoming Fake News and Echo Chambers in the Age of Social Media

In-house PR professionals, agency PR professionals and client-side marketers are known for their differences of opinion about the future of public relations. Key points that these stakeholders disagree and agree on are outlined in the Global Communications Report 2017, compiled by the USC Center for Public Relations and the Association of National Advertisers in consultation with their partner organizations. Here are five important insights drawn from the report and its associated research on The Evolution of Public Relations.

1. PR is becoming more important to marketing, even as both disciplines continue to converge

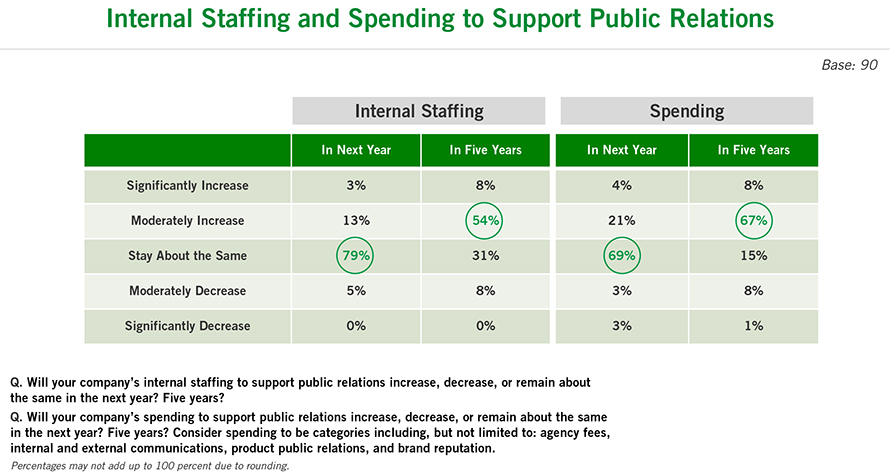

Client-side marketers plan to increase both internal staffing and overall spending on public relations over the next five years, according to ANA’s 2017 survey of U.S. marketers.

Increased spending suggests that public relations is “becoming more important to marketers”, said ANA’s Group EVP Bill Duggan, citing the crucial role for PR in managing digital communication and feedback loops.

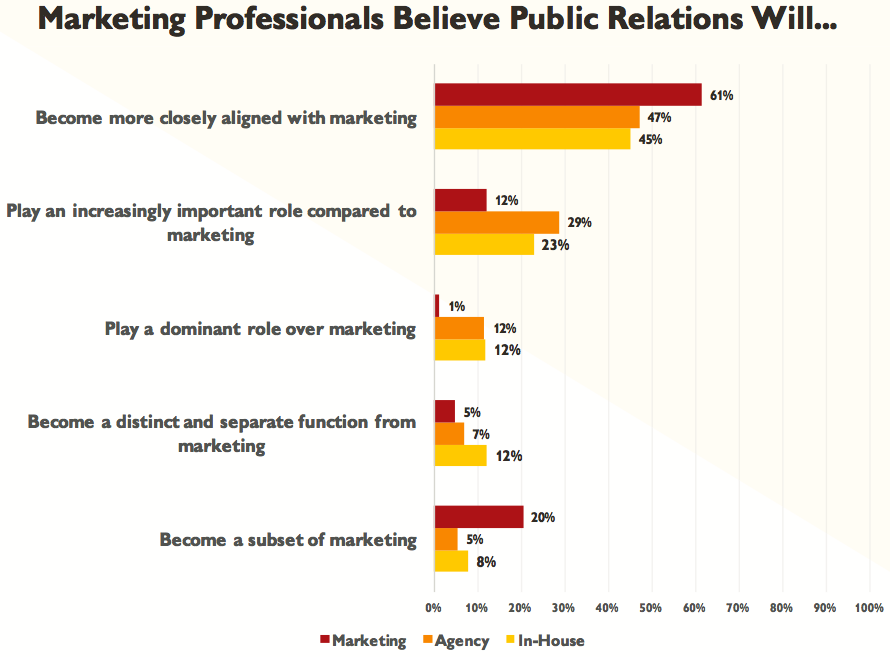

At the same time, a majority of surveyed marketers (61%) believed that PR will become more closely aligned with marketing, while 20% went so far as to say that PR will become a subset of marketing.

The global and U.S. PR professionals surveyed, however, were more hesitant about the convergence of PR and marketing. PR agency leaders indicated that they report most frequently into corporate communications (39%), which is more than into marketing (21%) or brand management (12%), but this gap is narrowing as client solutions become increasingly integrated.

Meanwhile, 18% of corporate communications departments were reporting into marketing. This proportion could grow if more organizations follow the example of Procter & Gamble, Virgin America and other well known companies by restructuring their marketing functions to include PR.

Whether convergence will expand or diminish the role of the PR professional is hotly contested. What does seem likely is that a broader skill set will be required to navigate the fluidity of marketing and PR in a digital world.

2. Declining revenues from earned media will put the spotlight on paid, shared and owned media – and the skills required to profit from them

PR agencies and in-house PR teams alike expect declining revenues from earned media over the next five years, prompting more spending on paid, shared and owned media.

Supporting this shift, over 60% of surveyed PR executives believed that branded content and influencer marketing, which are both primarily paid, will be important trends over the next five years.

Paid content, however, has long been the domain of advertising. PR professionals in a changing media landscape may benefit from mastering media buying, the report suggests, but this currently ranks last on the list of skills PR professionals consider important for future growth.

Meanwhile, more than half of the PR executives in the study believed that the consumer of the future will not distinguish between paid and earned media. Another one-third disagreed. The answer to this debate could have significant implications for all stakeholders.

3. PR professionals must harness social listening, digital storytelling, and social purpose

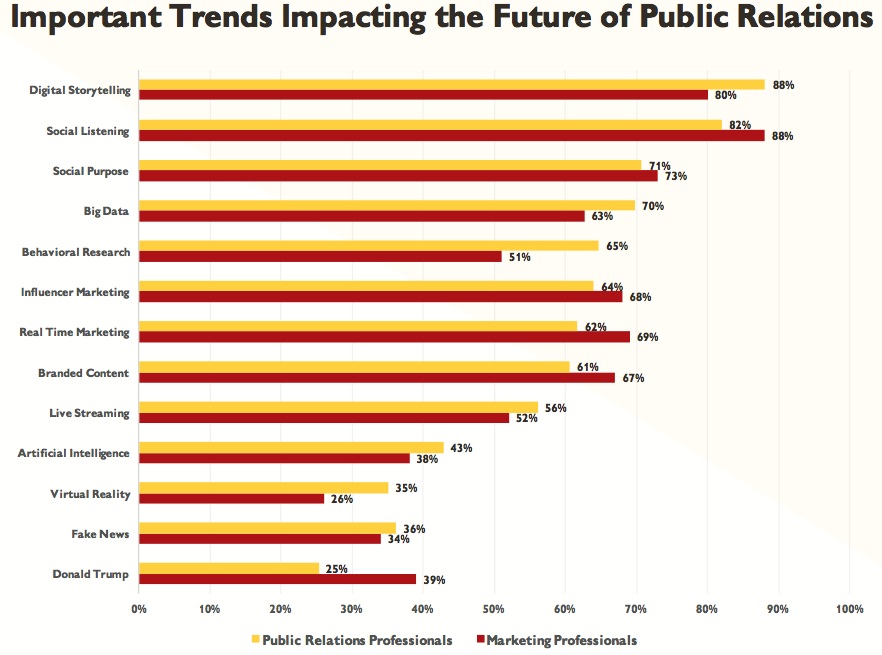

Digital can improve the quality of public relations by enabling instant outbound communication and inbound feedback. In this dynamic environment, PR professionals believe the most important trends impacting the future of the PR will be digital storytelling (88%), social listening (82%), social purpose (71%), and big data (70%).

Marketing professionals showed some consensus with PR professionals about these trends, but prioritized social listening (88%) over digital storytelling (80%), and real-time marketing (69%), influencer marketing (68%) and branded content (67%) over big data (63%).

Both groups agree on the importance of social purpose, which can be vital to the direction, cohesion and outcomes of the other top trends.

4. More clients will hire agencies to provide strategy, expertise, and creative thinking

The rising emphasis on strategy and creative in the client/agency relationship is a clear theme in both the 2016 and 2017 editions of the Global Communications Report.

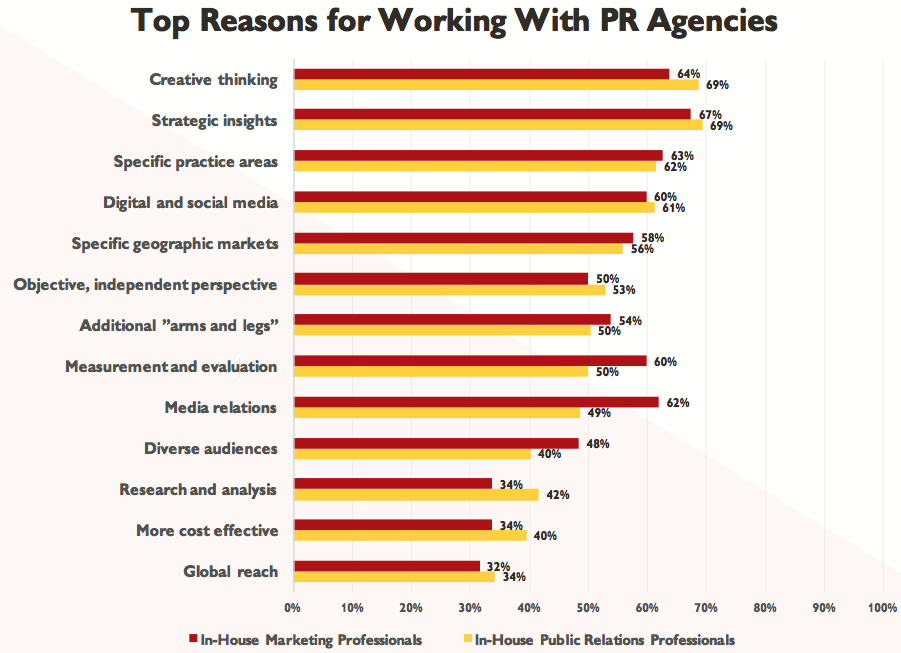

For the in-house marketing professionals surveyed in 2017, the top reasons for working with PR agencies were strategic insights (67%), creative thinking (64%), specific practice areas (63%), media relations (62%), digital and social media (60%), and measurement and evaluation (60%).

For in-house PR professionals, the top reasons for working with PR agencies were similar: strategic insights (69%), creative thinking (69%), specific practice areas (62%), and digital and social media (61%). However, there was less emphasis on measurement and evaluation (50%) and media relations (49%).

The growing strategic and creative input of PR agencies needs to be reflected in compensation models, says Fred Cook, Director of the USC Center for Public Relations, who suggests focusing more on value delivered than hours spent.

5. The value of PR will depend on achieving measurable business objectives

The vast majority of surveyed PR and marketing professionals believed that PR can best increase its value by demonstrating how PR programs achieve measurable business objectives.

However, improving measurement of results itself was a lower priority for PR in the eyes of PR professionals than marketing professionals, who, in turn, were less preoccupied about PR’s ability to address the wants and needs of all stakeholders. These disparities in stakeholder expectations can be reduced by establishing clear goals from the outset, as the report recommends.

The report also highlights the growing demand for PR to develop sophisticated ways to measure less-tangible variables like brand reputation, purchase intent, leadership, and creativity.

Repositioning PR to maximize relevance and talent

The five key insights above provide some clues as to how PR might reposition itself as an aspirational career choice – something which less than one-third of PR executives believe the industry is doing well. Given that recruiting and retaining the right talent remains a big challenge for PR, it will be interesting to see how the growing demand for strategic thinking – ranked in the study as the most important skill for today’s PR professionals – will shape PR in the years to come.

https://rossdawson.com/wp-content/uploads/2016/07/rdawson_1500x500_rgb-300x100.png00Vanessa Cartwrighthttps://rossdawson.com/wp-content/uploads/2016/07/rdawson_1500x500_rgb-300x100.pngVanessa Cartwright2017-06-14 13:19:282020-06-18 03:52:20The Changing Role of Public Relations: 5 Insights from the Global Communications Report 2017

One of the most striking trends in 21st century innovation is the significant potential for media to create value on a global scale.

Media, in all its forms, is fuelling economic growth, structural change, and technological advances like never before. As society debates the role and influence of media in a “post-truth” world, it is increasingly apparent that the future of media is crucial to shaping the future of humanity.

Media futurist Ross Dawson shared useful insights on how to create a vibrant future for media organizations in his keynote at the #SchibstedNext 2016 event held by Schibsted Media Group. You can see the video of the full keynote below.

Despite the widespread changes impacting the global media industry, Dawson pointed to the enduring and insatiable human appetite for information in a multichannel media world.

“Arguably the entire economy is becoming based on media, the creation of messages, the flow of messages, and where they are going,” Dawson said.

Here are six key ways in which media organizations can empower themselves to create their own future, drawn from Dawson’s talk at #SchibstedNext.

1. Create a compelling vision

“The best way to predict the future of media is to create it,” Dawson told the media leaders assembled in Oslo. For today’s media organizations, achieving a successful transition to tomorrow hinges on understanding “who it is we can be, who it is we want to be, moving forward”.

Forging a compelling vision for your media organization and communicating it effectively is vital for staff to adapt to the merging of technology and humanity, Dawson said, in an era when “technology is more and more capable, taking more and more of who we are”.

Without a clear strategic vision, companies are more likely to be blinded by past successes and overpowered by technological change. As the report of the 2020 group for the New York Times recently put it:

“To do nothing, or to be timid in imagining the future, would mean being left behind.”

2. Translate experimentation into value creation

Today, in the space of a day, you can test an idea, see how people respond, and develop it further. This has become a fundamental capability of every organization in the entire media industry.

“Revenue is highly uncertain, so you need to be able to experiment,” said Dawson. “For every experiment you should know what you want to learn, and when you learn that, you will be able to design the next experiment.”

Dawson referred to a basic test-and-learn model favored by entrepreneurs and outlined in The Lean Startup by Eric Ries: come up with an idea, put it into action, learn from that, iterate, and turn it into a result. “You can learn from others, absolutely, but you need to be able to create your own guidebook,” Dawson added.

Part of converting experimentation into value creation is a focus on community: “Being able to connect people, define what it is that’s common between them…to be able to create media which is relevant to all of those people, and to be able to filter that…to the individual…across many news or media organizations.”

3. Make the most of human and machine intelligence

Alongside advances in algorithms and the proliferation of convenient, high-tech user interfaces, robots and amateurs are now making music, art, video, and journalism in ways that were once limited to professionals. Dawson offered advice on how media organizations must respond:

“I believe that in the last 20 years, one of the most important things is how technology has enabled our creativity. If we are looking for the best media, we must bring together the professionals—who have the expertise and the context—with the amateurs, with all of us, with the many that are enabled by technology to create new possibilities.”

Optimizing both human and machine intelligence will become increasingly critical to value creation as organizations collect ever more data and achieve new milestones in consumer knowledge and engagement.

4. Ensure a clear and dynamic platform strategy

As existing and emerging media platforms vie for our attention, a solid understanding of platforms and their relationship to value creation is essential to steer media towards a positive future.

The best platform strategies, in Dawson’s view, are dynamic and user driven: “How is it you create value for participants? That’s the fundamental aspect of a platform,” he said. “Designing value for the participants in ways that they can create that together.”

In order to maximize value for participants across platforms, Dawson highlighted the role of data analysis, signal monitoring, user feedback loops, and collaboration with both internal and external platform creators.

5. Build on your existing capabilities and transcend their boundaries

A focus on transcending the boundaries has underpinned recent innovations in the media world, including the immersive virtual reality smartphone app available from the New York Times.

Media organizations must continue to think beyond the boundaries—such as print, broadcast, and even digital—if they are to create more compelling experiences for the audiences of tomorrow. Dawson elaborated:

“You need to be able to say, what are our capabilities today? What are we great at? What are we distinct at? What are we world-class at? What is it that we are going to build on? As organizations and individuals you need to be able to map your path and capability development moving forward.”

In order to transcend the boundaries and promote innovation, media brands are learning “to actually live what they are doing so that the messages that flow outside represent who they are,” said Dawson. This involves building the flow of communication and transparency internally in ways that mirror the external values and perceptions of a brand.

6. Foster bold and agile leadership to create your own future

Even as user participation in media continues to flourish, Dawson reminded the Schibsted audience that strong leadership remains crucial, because the future of media “is not a spectator sport.” As the Law of Requisite Variety makes clear, only those organizations that are as flexible as their environment will have the power to be able to create the future.

Therefore, leaders’ ability to put a bold vision into action, to push out the boundaries and set new standards for media will be crucial to success in the industry going forward. This is especially important because, at its core, the future of media “is an experiment,” Dawson believes.

“There is no roadmap to be able to say, this is exactly where the future of media is going. You need to create that. For your individual organization, it is going to be a different answer.”

https://rossdawson.com/wp-content/uploads/2016/07/rdawson_1500x500_rgb-300x100.png00Vanessa Cartwrighthttps://rossdawson.com/wp-content/uploads/2016/07/rdawson_1500x500_rgb-300x100.pngVanessa Cartwright2017-06-05 17:02:582019-03-01 11:17:276 Key Strategies Media Companies Need to Prosper in the Future News Industry

This website or its third-party tools use cookies to improve user experience and track affiliate sales. To learn more about why we need to use cookies, please refer to the Privacy Policy.

By clicking the agree button or continuing to browse through the website, you agree to the use of cookies. AcceptPrivacy Policy

Privacy & Cookies Policy

Privacy Overview

This website uses cookies to improve your experience while you navigate through the website. Out of these, the cookies that are categorized as necessary are stored on your browser as they are essential for the working of basic functionalities of the website. We also use third-party cookies that help us analyze and understand how you use this website. These cookies will be stored in your browser only with your consent. You also have the option to opt-out of these cookies. But opting out of some of these cookies may affect your browsing experience.

Necessary cookies are absolutely essential for the website to function properly. This category only includes cookies that ensures basic functionalities and security features of the website. These cookies do not store any personal information.

Any cookies that may not be particularly necessary for the website to function and is used specifically to collect user personal data via analytics, ads, other embedded contents are termed as non-necessary cookies. It is mandatory to procure user consent prior to running these cookies on your website.